Here is a list of books that I think are useful and interesting for any investor seeking to understand investing in emerging markets. The list reflects my bias for long-term investing rooted in knowledge of history and business cycles. I have included only books published in English, which is a big restriction. Also, I have not included basic investing books, which is an entirely sparate list.

The list is divided into three sections.

- Macro Economics and Business Cycles

- Development and Economic Convergence

- Regions and Countries

The books in each section are listed in no particular order.

1 Macro-economics, business-cycles and financial bubbles

The Volatility Machine by Michael Pettis

This Time is Different by Reinhart and Rogoff

The Bubble Economy by Chris Wood

Inflation and Monetary Regimes by Peter Bernholz

Money and Capital in Economic Development by Ronald McKinnon

How to Make Money with Global Macro by Javier Gonzalez

Business cycles: history, theory and investment reality by Lars Tvede

Emerging market portfolio strategies, investment performance, transaction cost and liquidity risk by Roberto Violi and Enrico Camerini II (Link)

Against the Gods by Peter Bernstein

Alchemy of Finance by George Soros

The Fourth Turning: What the Cycles of History Tell Us About America’s Next Rendezvous with Destiny by William Strauss, Neil Howe

Technological Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages by Carlota Perez

Extraordinary Popular Delusions and the Madness of Crowds by Charles Mackay

Manias, Panics, and Crashes: A History of Financial Crises, by Charles P. Kindleberger and Robert Z. Aliber

Devil Take the Hindmost: A History of Financial Speculation by Edward Chancellor

2 Development and Economic Convergence

Civilization and Capitalism, 15th-18th Century, Vol. I: The Structure of Everyday Life by Fernand Braudel

The Pursuit of Power: Technology, Armed Force, and Society since A.D. 1000 by William H. McNeill

The Wealth and Poverty of Nations: Why Some Are So Rich and Some So Poor by David S. Landes

Energy and Civilization: A History by Vaclav Smil

Barriers to Riches (Walras-Pareto Lectures) by Stephen L. Parente, Edward C. Prescott

The Great Convergence: Information Technology and the New Globalization

by Richard Baldwin

A Discussion of Modernization Li Lu (Link)

Slouching Towards Utopia?: AnEconomic History of the Long 20th Century, Brad Delong

Breakout Nations. In Pursuit of the Next Economic Miracles by Rushir Sharma

Why Nations Fail: The Origins of Power, Prosperity, and Poverty by Daron Acemoglu and James A. Robinson

The Wealth and Poverty of Nations: Why Some Are So Rich and Some So Poor by David S. Landes

The Birth of Plenty : How the Prosperity of the Modern World was Created by William J. Bernstein

Why Did Europe Conquer the World? by Philip T. Hoffman

Empire of Cotton: A Global History by Sven Beckert

The Pursuit of Power: Technology, Armed Force, and Society since A.D. 1000 by William H. McNeil

The White Tiger by Aravind Adiga

How to get Filthy Rich in a Rising Asia by Mohsin Hamid

AI Superpowers: China, Silicon Valley, and the New World Order by Kai-Fu Lee

Growth and Interaction in the World Economy by Angus Maddison

3 Regions and Countries

Latin America

Guide to the Perfect Latin American Idiot by Plinio Apuleyo Mendoza, Carlos Alberto Montaner, Alvaro Vargas Llosa

Left Behind: Latin America and the False Promise of Populism by Sebastian Edwards

Brazil

Brazil: A Biography by Lilia M. Schwarcz and Heloisa M. Starling

The Military in Politics: Changing Patterns in Brazil by Alfred C. Stepan

Brazillionaires: Wealth, Power, Decadence, and Hope in an American Country

by Alex Cuadros

Brazil: The Troubled Rise of a Global Power by Michael Reid

Lanterna na Popa by Roberto Campos

A Concise History of Brazil by Boris Fausto

A History of Brazil by E. Bradford Burns

Mexico

The Course of Mexican History by Michael C. Meyer and William L. Sherman

Mexico: Biography of Power. A History of Modern Mexico, 1810-1996 by Enrique Krauze

Turkey and the Middle East

The Political Economy of Turkey by Zulkuf Aydin

Midnight at the Pera Palace. The Birth of Modern Instanbul, by Charles King

The Prize: The Epic Quest for Oil, Money & Power by Daniel Yergin

The Yacoubian Building by Alaa Al Aswany

Russia

Wheel of Fortune. The Battle for Oil and Power in Russia by Thane Gustafson 2012

Red Notice: A True Story of High Finance, Murder, and One Man’s Fight for Justice by Bill Browder

The Future Is History: How Totalitarianism Reclaimed Russia by Masha Gessen

Asia

Asian Godfathers: Money and Power in Hong Kong and Southeast Asia by Joe Studwell

How Asia Works: Success and Failure in the World’s Most Dynamic Region

by Joe Studwell

Lords of the Rim by Sterling Seagrave

China

Factions and Finance in China by Victor C. Shih

Capitalism with Chinese Characteristics. Entrepreneurship and the State by Yasheng Huang

China’s Crony Capitalism: The Dynamics of Regime Decay by Minxin Pei

CEO, China: The Rise of Xi Jinping by Kerry Brown

Factory Girls: From Village to City in a Changing China by Leslie T. Chang

Avoiding the Fall. China’s Economic Restructuring by Michael Pettis

The River at the Center of the World by Simon Winchester

Mr. China by Tim Clissold

The China Strategy by Edward Tse

River Town by Peter Hessler

The Economic History of China: From Antiquity to the Nineteenth Century

by Richard von Glahn

Understanding China: A Guide to China’s Economy, History, and Political Culture

by John Bryan Starr

China’s Economy: What Everyone Needs to Know by Arthur R. Kroeber

Modern China by Jonathan Fenby

The Chinese Economy: Transitions and Growth by Barry Naughton

Wealth and Power. China’s Long March to the 20th Century by David Schell and John Delury

China’s New Confucianism by Daniel Bell

China Fireworks: How to Make Dramatic Wealth from the Fastest-Growing Economy in the World by Robert Hsu

Cracking the China Conundrum: Why Conventional Economic Wisdom Is Wrong

by Yukon Huang

Little Rice: Smartphones, Xiaomi, and the Chinese Dream by Clay Shirky

Alibaba: The House That Jack Ma Built by Duncan Clark

India

India – A Wounded Civilization by by V. S. Naipaul

Behind the Beautiful Forevers by Katherine Boo

India’s Long Road: The Search for Prosperity by Vijay Joshi

The Billionaire Raj: A Journey Through India’s New Gilded Age by James Crabtree

Capital: The Eruption of Delhi by Rana Dasgupta

Investing in India: A Value Investor’s Guide to the Biggest Untapped Opportunity in the World by Rahul Saraogi

Macro Watch:

India Watch:

- India’s strong economy leads global growth (IMF)

- (King coal rules India (Economist)

China Watch:

- China vs. the U.S.: the other deficits (Caixing)

- Media warns to avoid Japan’s mistakes (SCMP)

- China needs to get its house in order (SCMP)

- China resumes urban rail incestments (Caixing)

- Chinese firm will take over Iran gas project (Bloomberg)

China Technology Watch

- How WeChat conquered China (SCMP)

- Why do Western digital tech firms fail in China (AOM)

- Hayden Capital on China tech investments (HaydenCapital)

- A deep look into Alibaba’s 20F (Deep Throat)

- China’s rise in bio-tech (WSJ)

EM Investor Watch

- Turkey could be worse than Greece (dlacalle)

- The West’s broken relationsip with Turkey (Project Syndicate)

- Africa cannot count on growth dividend (FT)

Tech Watch

Investing

- Li Lu’s lecture at Beijing University (Himalaya Capital)

- Charlie Munger and Li Lu Interview (Guru Focus)

- Interview with Bill Nygren (Youtube)

- The 8 best predictors of market returns (WSJ)

India’s oil demand is expected to rise by 3.1% per year through 2040, from 5 million barrels/day to 9 million b/d. BP expects India’s oil production to decline slightly from the current 1 million b/d of production, so that demand growth will have to be supplied by imports, which will rise from 4 million b/d to about 8.2 million b/d. BP expects total global demand for oil to fall from 96 million b/d to 82 million b/d between 2017 and 2040, which means that India’s share of global oil demand will double from 5% to 10%. China’s oil demand is expected to rise from 13 million b/d to 15 million b/d, while production stays around 4 million b/d. This means Chinese imports would rise by 2 million b/d, from 9 million b/d to 11 million b/d, half as much in volumes compared to India. As India and China come to dominate the market for imported oil, both the U.S. and Europe will become less significant. The U.S. is expected to export 5 million b/d in 2040. Over this period, according to BP’s estimates, Europe’s import would fall from 11 million b/d to 7 million b/d. Where will India and China source their oil? In the chart below, the BP data points to the same primary sources that have met demand for oil imports in the past decades: Russia and the Middle East. China is already cementing its energy ties with Russia, building a series of pipelines to Siberia and importing Russian Artic liquid natural gas (LNG). India, on the other hand, has as its traditional supplier the Persian Gulf, which makes sense from a logistical point of view.

India’s oil demand is expected to rise by 3.1% per year through 2040, from 5 million barrels/day to 9 million b/d. BP expects India’s oil production to decline slightly from the current 1 million b/d of production, so that demand growth will have to be supplied by imports, which will rise from 4 million b/d to about 8.2 million b/d. BP expects total global demand for oil to fall from 96 million b/d to 82 million b/d between 2017 and 2040, which means that India’s share of global oil demand will double from 5% to 10%. China’s oil demand is expected to rise from 13 million b/d to 15 million b/d, while production stays around 4 million b/d. This means Chinese imports would rise by 2 million b/d, from 9 million b/d to 11 million b/d, half as much in volumes compared to India. As India and China come to dominate the market for imported oil, both the U.S. and Europe will become less significant. The U.S. is expected to export 5 million b/d in 2040. Over this period, according to BP’s estimates, Europe’s import would fall from 11 million b/d to 7 million b/d. Where will India and China source their oil? In the chart below, the BP data points to the same primary sources that have met demand for oil imports in the past decades: Russia and the Middle East. China is already cementing its energy ties with Russia, building a series of pipelines to Siberia and importing Russian Artic liquid natural gas (LNG). India, on the other hand, has as its traditional supplier the Persian Gulf, which makes sense from a logistical point of view.  Certainly, as they always have in the past, the geopolitics of oil will require that both India and China become much more involved in international politics. With the U.S. no longer importing oil from the Middle East and, perhaps, entering a period of lesser foreign-policy engagement, China and India will increasingly have to actively defend their strategic commercial interests. We have already seen this clearly wth regards to Indian imports of Iranian oil. India has increased its imports of Iranian oil sharply in recent years, and China and India are today Iran’s two biggest clients. Interestingly, both received waivers from the U.S. Iran sanctions and continue to buy Iranian oil. India’s dependence on oil imports with their highly volatile prices also will create greater macro-economic challenges. Growing oil imports may pressure the trade and current accounts. Unlike China, which experienced huge trade surpluses during its decades of dependence on the importation of oil and other commodities, India runs chronic current account deficits. These are likely to become more difficult to manage, leading to increased currency volatility. Trade Wars

Certainly, as they always have in the past, the geopolitics of oil will require that both India and China become much more involved in international politics. With the U.S. no longer importing oil from the Middle East and, perhaps, entering a period of lesser foreign-policy engagement, China and India will increasingly have to actively defend their strategic commercial interests. We have already seen this clearly wth regards to Indian imports of Iranian oil. India has increased its imports of Iranian oil sharply in recent years, and China and India are today Iran’s two biggest clients. Interestingly, both received waivers from the U.S. Iran sanctions and continue to buy Iranian oil. India’s dependence on oil imports with their highly volatile prices also will create greater macro-economic challenges. Growing oil imports may pressure the trade and current accounts. Unlike China, which experienced huge trade surpluses during its decades of dependence on the importation of oil and other commodities, India runs chronic current account deficits. These are likely to become more difficult to manage, leading to increased currency volatility. Trade Wars

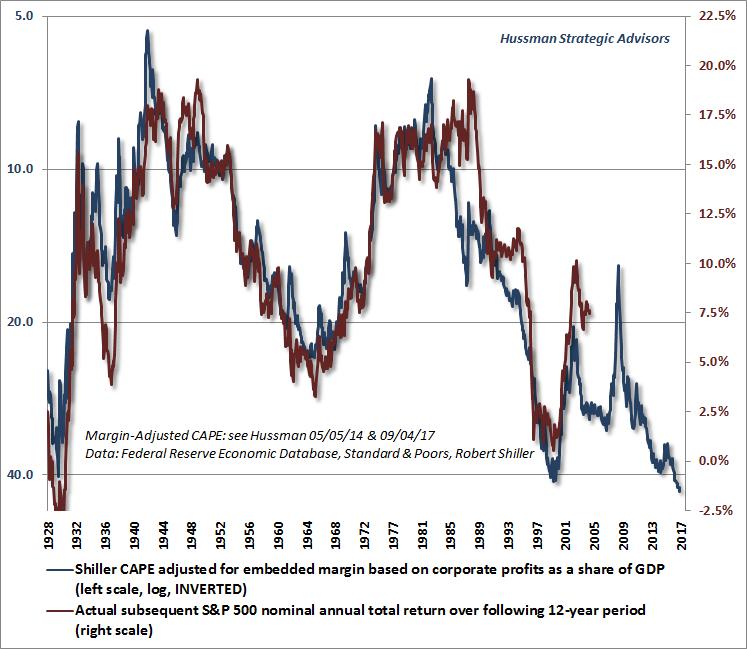

We can look at relative valuations to explain this relative performance. The chart below looks at Cyclicaly Adjusted Price-earnings (CAPE) ratios for both EM and the S&P 500. (The CAPE takes an average of ten-year inflation-adjusted earnings to smooth out cyclicality). This poor EM performance occurred because at the beginning of the period valuations in EM were relatively high and U.S. valuations were relatively low.

We can look at relative valuations to explain this relative performance. The chart below looks at Cyclicaly Adjusted Price-earnings (CAPE) ratios for both EM and the S&P 500. (The CAPE takes an average of ten-year inflation-adjusted earnings to smooth out cyclicality). This poor EM performance occurred because at the beginning of the period valuations in EM were relatively high and U.S. valuations were relatively low.  The chart shows that a year-end 2008 EM was trading at a CAPE multiple 0f 14.7, in line with its 15-year average. Meanwhile, the U.S. market was valued at a CAPE mulitple of 15x, compared to its 15-year average of 26x. By the end of the 10-year period, EM CAPE multiples had declined and were well below historical averages while U.S. multiples were well above the historical average. This largely explains the relatively strong returns of the S&P 500 for the 2008-2018 decade. As a reminder, the previous decade 1998-2008 had been an entirely different story, with EM vastly outperforming the stagnant U.S. market. During the 1998-2008 period, EM CAPE multiples expanded and U.S. mulitples contracted. In fact, if we look at the past twenty years EM stock market performance is far ahead , providing returns of 444% vs. 204% for the S&P 500, as shown in the gaph below.

The chart shows that a year-end 2008 EM was trading at a CAPE multiple 0f 14.7, in line with its 15-year average. Meanwhile, the U.S. market was valued at a CAPE mulitple of 15x, compared to its 15-year average of 26x. By the end of the 10-year period, EM CAPE multiples had declined and were well below historical averages while U.S. multiples were well above the historical average. This largely explains the relatively strong returns of the S&P 500 for the 2008-2018 decade. As a reminder, the previous decade 1998-2008 had been an entirely different story, with EM vastly outperforming the stagnant U.S. market. During the 1998-2008 period, EM CAPE multiples expanded and U.S. mulitples contracted. In fact, if we look at the past twenty years EM stock market performance is far ahead , providing returns of 444% vs. 204% for the S&P 500, as shown in the gaph below.  So, what can current valuations tell us about probable future returns? In short, the prospects look good for EM. EM is now relatively cheap, trading at a CAPE valuation of 11.7 vs. a 15-year average of 16. Meanwhile, U.S. stocks trade at a CAPE of 28.4 times vs. an average of 24.7x. The U.S. dollar has also been strengthening for years against EM currencies, a trend that is likely to revert in the future. Though, in the words of baseball legend Yogi Berra, “it is difficult to make predictions, especially about the future”, we can use the historical context to make some guesses about probable future returns. We make three assumptions: 1. Valuations will move back to the historical CAPE average over the next five years; 2. Earnings return to historical trend; and 3. Normalized earnings grow by nominal GDP. To determine the historical earning trend we take a view of where we are in the business-earnings cycle. In the case of EM we consider that at this time earning are about 10% below trend and we assume 6.5% nonimal GDP Growth (vs. 4% for developed markets). Based on this simple framework and assumptions we project annualized returns for EM stocks for the next five years of 9.8% (9.3% for ten years). Adding dividends, we project total annualized returns of 12.1% (10.5% for ten years.) The U.S. ,by contrast, is likely to experience multiple contraction and is at peak earnings, so that returns can be expected to be low single-digits. Two outside opinions shown below arrive at similar results: first GMO (on the left) projects 4.4% real annualized returns for EM (7.9% for EM value) for its seven-year forecast period; Research Affiliates (

So, what can current valuations tell us about probable future returns? In short, the prospects look good for EM. EM is now relatively cheap, trading at a CAPE valuation of 11.7 vs. a 15-year average of 16. Meanwhile, U.S. stocks trade at a CAPE of 28.4 times vs. an average of 24.7x. The U.S. dollar has also been strengthening for years against EM currencies, a trend that is likely to revert in the future. Though, in the words of baseball legend Yogi Berra, “it is difficult to make predictions, especially about the future”, we can use the historical context to make some guesses about probable future returns. We make three assumptions: 1. Valuations will move back to the historical CAPE average over the next five years; 2. Earnings return to historical trend; and 3. Normalized earnings grow by nominal GDP. To determine the historical earning trend we take a view of where we are in the business-earnings cycle. In the case of EM we consider that at this time earning are about 10% below trend and we assume 6.5% nonimal GDP Growth (vs. 4% for developed markets). Based on this simple framework and assumptions we project annualized returns for EM stocks for the next five years of 9.8% (9.3% for ten years). Adding dividends, we project total annualized returns of 12.1% (10.5% for ten years.) The U.S. ,by contrast, is likely to experience multiple contraction and is at peak earnings, so that returns can be expected to be low single-digits. Two outside opinions shown below arrive at similar results: first GMO (on the left) projects 4.4% real annualized returns for EM (7.9% for EM value) for its seven-year forecast period; Research Affiliates ( On a country-by-country basis, as one would expect, great differences appear. Countries find themselves at different points in the business-earnings cycle and their valuations may vary greatly depending on the mood and perceptions of investors. The chart below shows where country-specific valuations stand relative to the 15-year CAPE average for the primary EM markets. The third column shows the difference between the current CAPE and the historical average. For example, Turkey’s valuation, in accordance with CAPE, is 60% below normal. The markets in the chart are ranked in terms of probable long-term returns (5-10 years), with the last two columns to the right estimating annualized total returns (including dividends) for the next five and ten years. The table also shows where markets are currently in their business-earnings cycle and expected annualized earnings growth for the next five years.

On a country-by-country basis, as one would expect, great differences appear. Countries find themselves at different points in the business-earnings cycle and their valuations may vary greatly depending on the mood and perceptions of investors. The chart below shows where country-specific valuations stand relative to the 15-year CAPE average for the primary EM markets. The third column shows the difference between the current CAPE and the historical average. For example, Turkey’s valuation, in accordance with CAPE, is 60% below normal. The markets in the chart are ranked in terms of probable long-term returns (5-10 years), with the last two columns to the right estimating annualized total returns (including dividends) for the next five and ten years. The table also shows where markets are currently in their business-earnings cycle and expected annualized earnings growth for the next five years.  What does this table tell us? First, we can see that valuations are generally low. The majority of markets in EM trade at very deep discounts. India, Peru and Thailand, the most expensive markets, are valued only slightly above historical valuations and are not abnormally high in absolute terms. Second, most markets stand in the early-to-mid part of the earnings cycle. This provides the opportunity for concurrent earnings growth and multiple expansion for Brazil, China, Chile, Mexico, Malaysia, Colombia and Turkey. What does the table not tell us? First, this methodology serves best as a long-term allocation tool, not as a timing tool. Market timing is difficult because short-term stock movements are determined much more by liquidity considerations and the mood of investors than by valuation. So, for example, timing a stock market recovery in Turkey is not easy. The market may fall much further before it starts a recovery. Eventually, a new more constructive narrative will gain traction in Turkey and catch the attention of investors, starting a new cycle. Second, the assumptions of the model may be wrong.

What does this table tell us? First, we can see that valuations are generally low. The majority of markets in EM trade at very deep discounts. India, Peru and Thailand, the most expensive markets, are valued only slightly above historical valuations and are not abnormally high in absolute terms. Second, most markets stand in the early-to-mid part of the earnings cycle. This provides the opportunity for concurrent earnings growth and multiple expansion for Brazil, China, Chile, Mexico, Malaysia, Colombia and Turkey. What does the table not tell us? First, this methodology serves best as a long-term allocation tool, not as a timing tool. Market timing is difficult because short-term stock movements are determined much more by liquidity considerations and the mood of investors than by valuation. So, for example, timing a stock market recovery in Turkey is not easy. The market may fall much further before it starts a recovery. Eventually, a new more constructive narrative will gain traction in Turkey and catch the attention of investors, starting a new cycle. Second, the assumptions of the model may be wrong.

{kind=link}