Emerging markets have come out of a period of considerable underperformance relative to both the U.S. market and international developed markets. They have now outperformed for over two years, recovering some lost ground.

Valuations in emerging markets remain in line with historical norms, which is an aberration in a world of generally extreme asset prices. Strangely, while a very large growth premium is paid for growth assets in the U.S. market, that view has not benefited emerging markets, even though on average they have much higher GDP growth than developed markets.

EM’s poor performance over the past decade can largely be attributed to multiple contraction (The Past Ten Years in Emerging Markets). The graph below shows the evolution of the cyclically adjusted price to earnings (CAPE) ratio over this period. The average historical CAPE ratio for EM has been 14.4, which is exactly in line with the current level. After peaking in 2007, the CAPE for EM bottomed out in 2011-2013, at 10 times trailing earnings. We have already seen considerable multiple expansion since then, a consequence of the past two years of strong performance. Nevertheless, we can expect that, as always, valuations will peak this cycle well above the historical average, so additional multiple expansion is likely.

On a country-by-country basis, however, greater opportunities exist, and the investor can weigh his allocations accordingly. The chart below shows how valuations have evolved over the past ten years for the primary EM countries. The first two columns on the left show the CAPE ratios at year-end 2007 and 2017, respectively. While the U.S. saw multiple expansion, every EM country saw multiple contraction over this period. The next to last column on the right shows the country’s average CAPE for the past twenty years, and the last column shows how far the 2017 ratio is above or below the average.

Several conclusions can be drawn from this table.

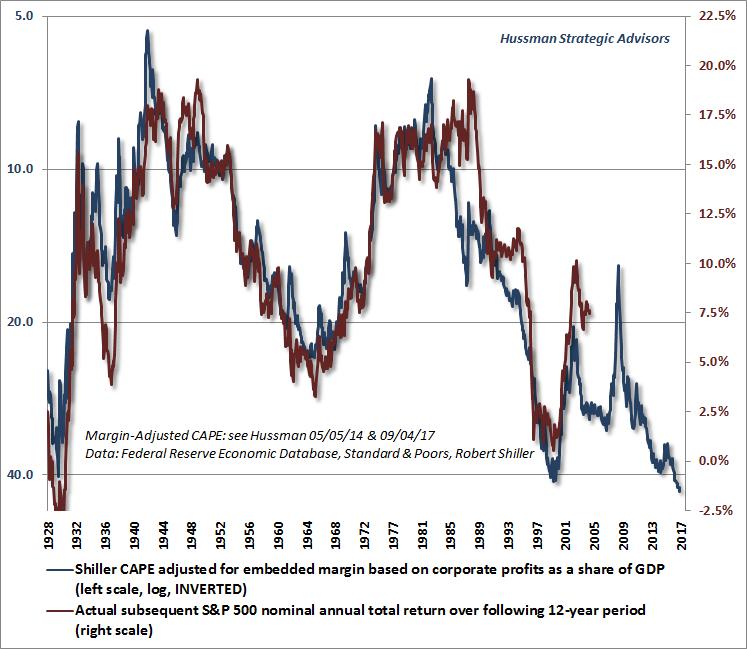

- The U.S market is priced for perfection, and should be expected to provide very low returns for the next 7-10 years.

- “Risky” countries (commodity producers and those dependent on erratic foreign flows) offer significant upside to get back to average valuations. These “boom-to-bust” markets now stand to benefit from late-cycle effects of the U.S. economy, the weak dollar and strengthening commodity prices and will eventually trade at multiples above the historical average. This means high potential upside for stock prices in Russia, Brazil, Turkey, Malaysia , Chile and Colombia.

- Mexico has been overly punished because of concerns with President Trump and the 2018 presidential election, and it could rebound strongly.

- Indonesia and India are near normal valuations, and will need strong earnings growth and higher multiples to continue to outperform.

- Philippines is at a very high level of valuation. This “FIRE” (finance-insurance-real estate) economy/market has benefited from liquidity and low interest rates, as these activities are all highly leveraged. Of course, the opposite will occur on the downside.

Valuations, in general, and CAPE in particular, are not good timing tools. However, historical observation and the academic research done by Professor Robert Shiller and others show a high correlation between CAPE and future returns. In EM, investors are fickle and nervous and things tend to happen quicker than in developed markets, so CAPE is probably a good allocation tool for 3-5 year investment cycles.

India Watch:

- India’s manufacturing challenge (India Times)

- Modi at Davos (Economic Times)

China Watch:

- Couples not delivering on babies (Caixing)

- The world’s most valuable luxury good company (WIC)

- Making China Great Again (The New Yorker)

China Technology Watch:

- China now top producer of scientific articles (Nature)

- Tencent’s Wechat: an app and an app-store at the same time (SCMP)

- China to test new Maglev train (Caixing)

- JD’s Liu goes to Davos (SCMP

- Smartphone sales fall in China for the first time (SCMP)

- Xiaomi gains top smartphone spot in India (SCMP)EM Investor Watch:

Technology Watch:

- Amazon’s new Go store (Stratechery)

- Renewable power costs in 2017 (Irena)

- Apple’s share of smartphone profits is falling (SCMP)

Investor Watch:

- Ben Carson on market drawdowns (Wealth of Common Sense)

- An interview with Ed Thorpe (http://AQR)

- Tech will revolutionize institutional investment (Institutional Investor)

- Shiller on CAPE ratios (Project Syndicate)

- Shiller on narrative (Chicago Booth)

- My favorite performance chart (Wealth of Common Sense)

- U.S. future equity returns (Philosophical Economics)

- The Seven deadly sins (Mauldin Economics)

{kind=link}